Jessica Skolnick, CFA, Director of Investments

Adam Bernstein, ESG Analyst

Macro and Markets Update

As we pass the halfway point of the final quarter of 2023, we find ourselves in another risk-on rally fueled by hopes of an imminent soft landing accompanied by sooner-than-expected rate cuts by the Federal Reserve. The sentiment is a sharp reversal from where we were last month when we published our last commentary. The S&P 500 lost ground in August, September, and October,1 the longest monthly losing streak since early 2020. The 10-year Treasury yield had risen in each of the previous 6 months through the end of October and briefly touched the key 5% level on October 19th.2 Markets seemed to be accepting the Fed’s message of higher-for-longer rates and processing the implications of that on asset prices.

The FOMC meeting on November 1st turned the market’s frown upside down, though we are not sure anything has really changed. As expected, the Fed left the Fed Funds rate stable at 5.25%-5.50% and released a statement upgrading economic growth from “solid” to “strong”, acknowledging moderation in a still-strong labor market and indicating that the rise in long-term rates exerted some financial tightening in addition to their monetary policy tightening effects.3 Fed Chair Jerome Powell made it clear in the post-meeting press conference that rate cuts are not part of the discussion, since inflation remains above the Fed’s 2% target: “The Committee is not thinking about rate cuts right now at all. We are not talking about rate cuts.”4

The market glossed over Powell’s statements and immediately began pricing in additional rate cuts in 2024, widening the gap between the Fed’s dot plot and market forecasts even further. The median dot plot projection for year-end 2024 is 5.125% (implying one rate cut), while the market’s forecast is just 4.41%, indicating nearly four rate cuts in the next 13 months!5 Stock and bond markets did what they have done every time a phantom pivot has been priced in. The 10-year fell from 4.93% on the morning of the Fed meeting to 4.64% on November 13th, and the yield curve inversion between the 2-year and 10-year Treasury more than doubled from 15 bp to 40 bp, while the S&P 500 rallied nearly 5% over this same timeframe.

Meanwhile, nothing much has changed in the underlying data or in the Fed speak following the meeting. The labor market has weakened slightly but remains strong by historical metrics. Job openings were at 9.5 million in September, compared to a 5 million average in the decade preceding the Covid pandemic.6 The September non-farm payroll report was a bit weaker than expected, primarily due to ongoing labor strikes rather than layoffs or other signs of reduced labor demand. October Consumer Price Inflation moderated to 3.2%, but the core measure remained elevated at 4.0%,7 twice the Fed’s target, and the November University of Michigan survey showed short and long-term inflation rose to the highest levels in over a decade.8

The Fed may stay in an extended pause given the precipitous fall in long-term rates, little indication of a growth slowdown and falling inflation that remains above target, but the catalysts for actual rate cuts are absent. Premature rate cuts against a solid economic backdrop risk a reacceleration in inflation that the Fed wants to avoid. A hard landing scenario in which rate cuts are necessary would not support the risk-on sentiment currently present in the market.

ESG Update – Divergent Energy Views

- International Energy Agency:

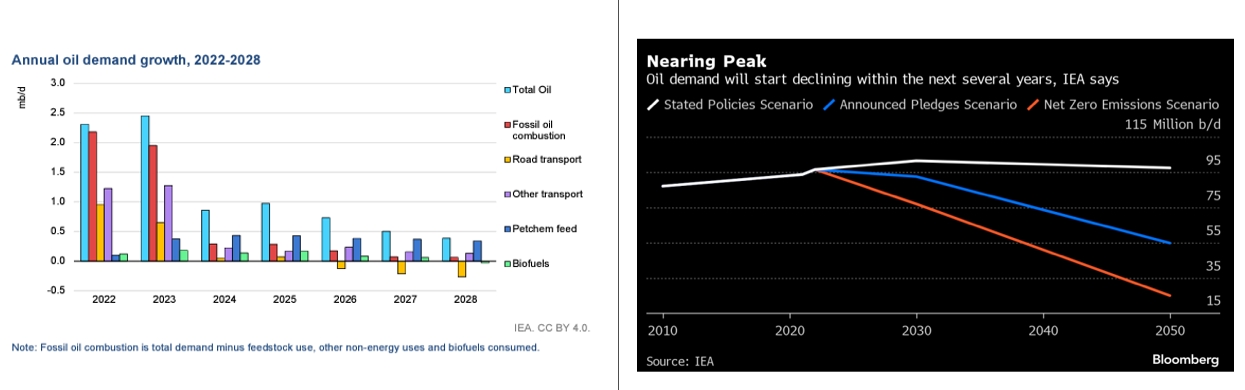

The International Energy Agency (IEA) just released its 2023 World Energy Outlook report that predicts, for the first time, that global oil demand will reach its peak this decade. The predicted peak for oil, which also extends to cover coal and natural gas, does not mean a rapid plunge is imminent, but the IEA forecasts a downward slopping plateau over several years.9

Source: IEA, Bloomberg

The IEA prediction hinges on a few key assumptions:

- The economics of the energy transition are gaining momentum. The Levelized Cost of Electricity (LCOE) is a metric used to estimate the average cost of generating one unit of electricity. It is a useful measure for comparing the cost-effectiveness of different energy sources or technologies. It depends on the asset and location but generally, solar, on-shore/off-shore wind, and geothermal energy production have cheaper LCOE pricing than traditional energy sources, such as coal and gas, and this trend is accelerating.

- Demand for oil in petrochemicals, aviation, and shipping will likely continue to increase until at least 2050, but this increase in demand will be more than offset by the lower oil demand for transport as the growth in electric vehicles continues to rise.10

- China is expected to represent about 40% of global oil demand in 2023.11 Said another way, China holds the key to shifting global energy demand. China’s oil demand is facing structural decline, due to record growth in the installation of new low-carbon energy sources.

- Organization of Petroleum Exporting Countries (OPEC):

OPEC predicted in their 2023 annual outlook that oil demand will continue to grow for decades, reaching 116 million barrels a day in 2045. This prediction represents a 16% increase in demand and 6 million barrels a day more than previously predicted. To reach these numbers, OPEC has India more than doubling its consumption, and China increasing oil demand by 26%.12 - Big U.S. Oil:13

U.S. supermajors are also taking a dissenting stance. ExxonMobil’s recent venture into acquiring shale producer Pioneer Natural Resources and Chevron’s latest deal to absorb Hess mark a substantial consolidation within the Big Oil landscape, a scale not witnessed in two decades. These corporate unions seem to challenge the International Energy Agency’s (IEA) prognosis of a shrinking demand for oil, or, at the very least, position these expanded U.S. giants strategically as the enduring producers poised to meet the anticipated demand lingering into the mid-century. By reaffirming their commitment to oil, U.S. corporations are accentuating the growing gap with their European counterparts, who are cautiously tiptoeing into the realm of clean energy initiatives.

- Organization of Petroleum Exporting Countries (OPEC):

Supermajors grapple with marketing a declining product but strive to be among the last standing. Anticipating reduced demand, they focus on being low-cost providers, making these deals viable even in a shrinking market. The production cost curve in commodities implies that if your cost of production is low enough, your risk is minimal. Businesses who operate in the oil & gas sector are used to earning certain return profiles. Renewables, however, tend to be both lower return and lower risk, which is a big reason why oil companies do not see the logic in diversifying much into clean energy. Another way these oil giants might look to play on the energy transition is to invest in heavy metal mining, a business with more similar risk/return metrics. “Exxon Mobil Corp. plans to become one of the biggest suppliers of lithium for electric vehicles, marking the oil giant’s first major foray outside of fossil fuels in decades. Exxon aims to produce its first lithium by 2027 and ramp up output to the equivalent of 1 million electric vehicles annually by 2030.”14 Consolidations do not guarantee faith in the growth of an industry, true confidence lies in investing in a sectors riskier market’s. Limited appetite is evident, even among those predicting prolonged oil demand.

- Gitterman’s In-House View

We were experiencing rising global energy demand and declining supply, which manifested in surging prices, grid failures, and rolling blackouts around the world, even before the Covid pandemic and the Russia-Ukraine War. In most places where we are producing oil (OPEC, Russia, US, Brazil), the amount we are producing is dropping. We have already depleted the best oil fields and well depletion math only accelerates as we go to lesser fields. Oil demand will likely peak in the short-term, but global energy demand is still accelerating and has grown by about 2% per year since 1973. The best way to limit the effects of a warming climate to levels that sidestep the worst physical effects is to decarbonize our energy generation mix.

In the intermediate term, non-OPEC+ countries dominate medium-term capacity expansion plans, led by the United States, Brazil, and Guyana. The relatively strong increases from non-OPEC+ producers, together with the projected slowdown in demand increases the spare capacity for oil in the intermediate term, keeping energy prices in check. Many investors are overlooking the underestimated risks tied to a sustained rise in commodity price inflation. Capital limitations and the depletion of resources are poised to propel prices upward in the years ahead, contrary to the trends of the past decade. Consequently, investors remain hesitant to fully embrace the potential implications of this shift. We think the “end of oil” will be a function of price-related demand destruction, not technology-driven obsolescence (even though the cost curves for renewable power will help). Before we get there, we are likely to see marginal producers bought by lower cost providers with scale until it is harder and more expensive to transport traditional energy around the grid than renewable sources.

- All performance figures are total return and sourced from Bloomberg as of 11/14/2023. ↩

- US Generic Govt 10 Yr Index, Bloomberg, as of 11/14/2023 ↩

- US Federal Open Market Committee statement, 11/1/2023, Federal Reserve Board and Bloomberg News ↩

- Transcript of Chair Powell’s Press Conference 11/1/2023, Federal Reserve, https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20231101.pdf ↩

- Bloomberg, Implied Fed Funds Target Rate, FOMC Dot Plot, as of 11/14/2023 ↩

- US Job Openings by Industry Total SA. Bloomberg, Bureau of Labor Statistics, as of 11/14/2023 ↩

- US CPI Urban Consumers YoY NSA, Bloomberg, Bureau of Labor Statistics, as of 11/14/2023 ↩

- UMich Expected Change in Prices During the Next Year, UMich Expected Change in Prices During the Next 5-10 Years, Bloomberg, University of Michigan, November 2023 Preliminary, as of 11/14/2023 ↩

- “Oil 2023.” IEA, June 2023, www.iea.org/reports/oil-2023#downloads ↩

- “Oil 2023.” IEA, June 2023, www.iea.org/reports/oil-2023#downloads ↩

- https://www.cnbc.com/2023/03/23/wood-mackenzie-chinas-oil-demand.html#:~:text=Asia%20Markets-,China%20will%20make%20up%20nearly%2040%25%20of%20the%20rise%20in,in%202023%2C%20Wood%20Mackenzie%20says&text=%E2%80%9CA%20return%20to%20normal%20mobility,Mackenzie%20said%20in%20a%20report. ↩

- OPEC Boosts Oil Demand Forecast to 2045 Despite Climate Crisis. Bloomberg, 10/9/2023 ↩

- https://www.ft.com/content/02fb0da4-a834-4ac5-80f0-a0107596bd37 ↩

- https://www.bloomberg.com/news/articles/2023-11-13/exxon-aims-to-become-a-leading-lithium-supplier-for-evs-by-2030#xj4y7vzkg ↩